A Brief History of North American Power Grid

A review of the development of the North American power grid over the past century, and the critical milestones and events that influences its development can help to 1) explain the current state of the market, 2) reveal inefficiencies and contextualize opportunities, and 3) demonstrate market, technical, and regulatory trends.

This is the first article of a three part series. Click here to view the second part of this series Defining Trends in the Power Markets, and click here to view the third part of this series A North American Power Platform.

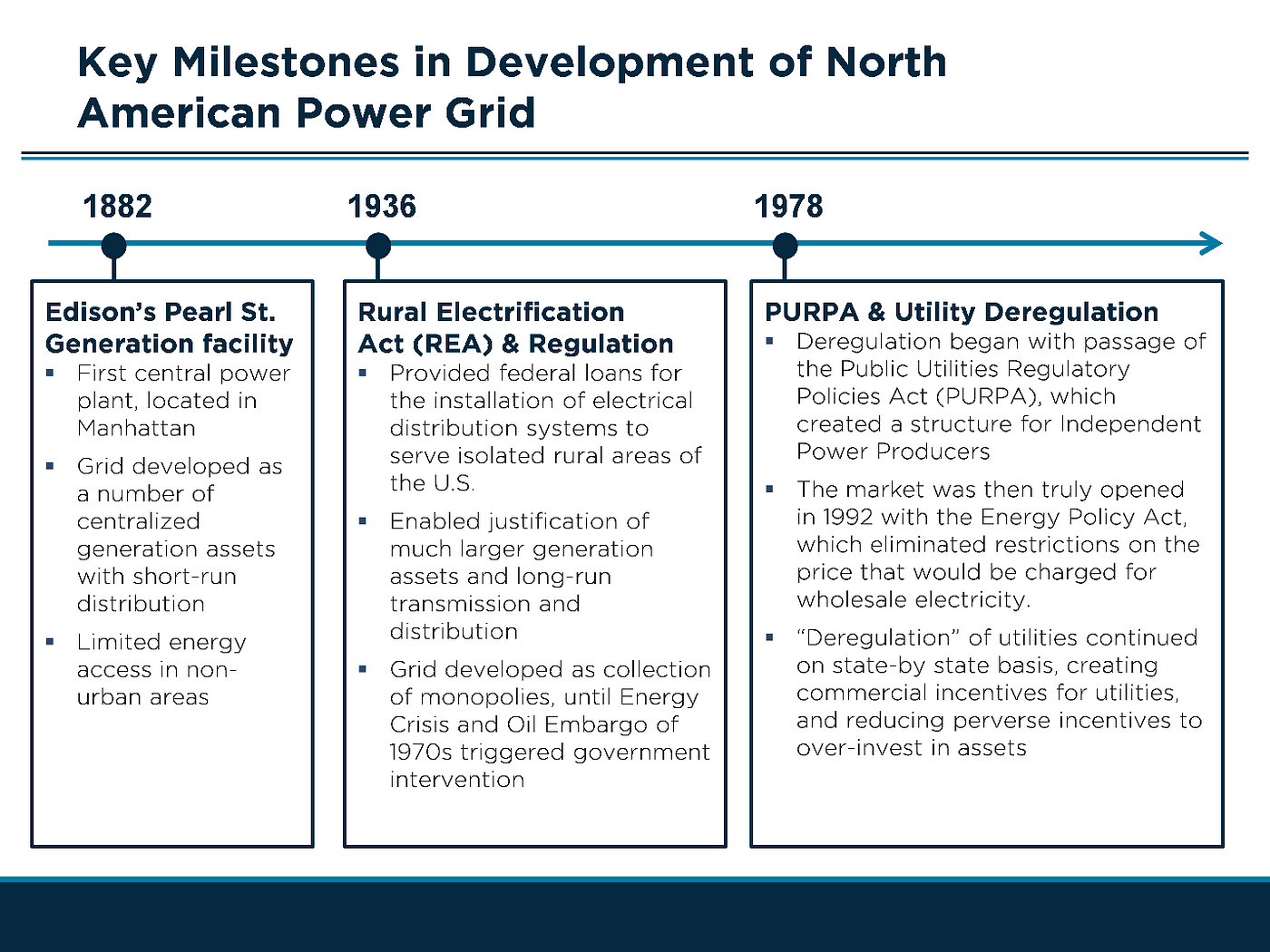

Milestones in History of Power Generation, Transmission, and Distribution

Early Electric Power Systems, the Early Power Grid, and Rural Electrification Act

As demonstrated in the timeline above, beginning in 1882, the North American power market initially developed with small, isolated, and centralized thermal (coal-fired) generation assets, which primarily served densely populated, urban markets with short-run distribution. The independent generators were unregulated and often competed for the same customers. As some of these early power systems expanded, it became possible to connect previously isolated systems over large geographic areas, thereby allowing neighboring systems to share generation and voltage stability resources. Despite the risk of shared disturbances inherent in an interconnected grid, interconnections began to expand rapidly by the 1920s.

By the 1930s, nearly ninety percent (90%) of urban residents had access to electricity, although only ten percent (10%) of rural residents, including farmers, had access to electricity. In May of 1936, the Roosevelt Administration issued the Rural Electrification Act to address this disparity, providing federal loans to cooperative electric power companies for the installation of electrical distribution systems to serve isolated rural areas. With increasing electricity demand in North America and the passing of the Rural Electrification Act (REA) in 1936, utilities began to build larger power plants, reducing the cost of generation and distribution, and expanding the utility rate base. By 1939, just three years later, the percentage of rural households with electricity had risen to 25 percent. By 1953, more than ninety percent (90%) of farms across the nation had electricity. These member-owned cooperatives (most still exist today) purchased power on a wholesale basis and distributed it using their own network of transmission and distribution lines. The figure below demonstrates the immediate expansion of member-owned cooperatives after the Rural Electrification Act.

Grid Map for Member-Owned Cooperatives, Pre- and Post- REA

Source: National Rural Electric Cooperative Association.

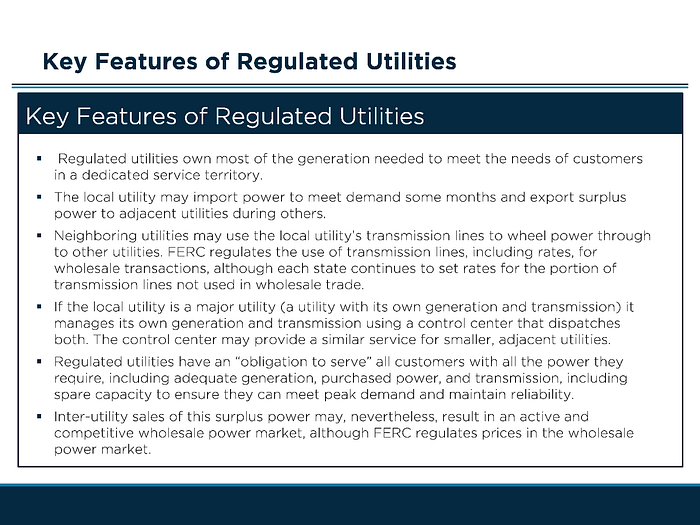

Regulated Utilities

To reduce redundancies in the grid, regional monopolies developed (with utilities owning all of the generation (i.e., power plants), transmission, and distribution assets in their territory of operations. Samuel Insull was a pioneer of this model, forming Commonweath Edison in Chicago through the consolidation of twenty different power companies, demonstrating the favorable economics for large energy companies. Without regulation, these utilities had vertical market power, and could overcharge customers due to lack of competition and inelastic market demand. Consequently, state Public Utilities Commissions (PUCs) were developed to regulated retail electricity prices within their state to protect customers from monopolistic pricing, and the Federal Energy Regulatory Commission (FERC) was developed to regulate wholesale electricity prices.

In the regulated model, regulators set a rate of return of profits for utilities based on the cost of service (thus “decoupling” utility profits from the price of electricity). The rate of return was set to allow utilities to earn a profit and attract capital from investors by providing a return on the utilities’ capital investments and operating expenses. Rates were determined by periodic rate cases, in which state PUCs assess utilities’ current and forecasted expenses. This model, used by both municipal utilities and rural electric cooperatives, was created to encourage infrastructure investments during a period of significant growth in electricity demand per capita and population.

Until the 1970s, increased demand for electricity among consumers and reduction in the cost of generation (with increasing utility generation asset scale) resulted in low-cost, abundant power. Utilities routinely requested lower rates in order to broaden their rate base, as the cost of production decreased. This trend ended dramatically with the Arab Oil Embargo in the 1970s and the energy and fuel price volatility that ensued.

Characteristics of Regulated Utilities

Source: U.S. Department of Energy, 2002.

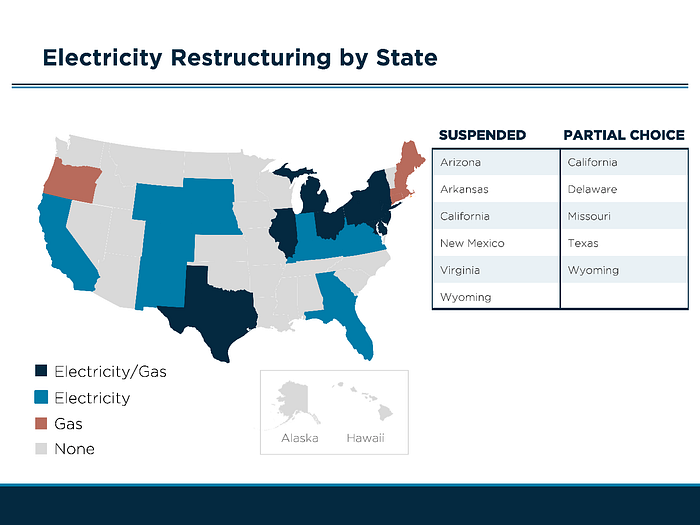

Utility Deregulation and Public Utilities Regulatory Policies Act (1973 — Current)

In response to the Oil Embargo and resulting volatility and escalation of global energy prices, utilities began to build large-scale coal and nuclear plants to reduce dependency on foreign energy markets. This in turn increased utility costs dramatically, and created an opportunity for Independent Power Producers (IPPs) to build small-scale plants to take advantage of unique generating opportunities such as co-generation (of power and steam), renewable resources, and municipal waste utilization. In 1978, as part of the National Energy Act, the federal government issued the Public Utility Regulatory Policies Act (PURPA), which required utilities to buy power from qualifying non-utilities at the utility’s avoided cost, thereby guaranteeing these non-utilities a market for the electricity. The unintended result of this act was enabling competition in the wholesale electricity markets to nonutility producers. The Energy Policy Act of 1992 (EPACT) further encouraged competition by 1) creating a new class of nonutility generators (i.e., Independent Power Producers) that were exempt from some corporate ownership and geographic restrictions and 2) requiring public utilities to provide open access to the U.S. power transmission grid.

The growth of IPPs and inefficiencies of the rate setting system led to a surge of state-level restructuring activity. In 1996, California and Rhode Island passed landmark legislation to restructure their power industries and give their consumers the right to choose their electricity supplier. Since then, an increasing number of state-level policies have been issued to allow for some level of competition in electricity and natural gas markets. Several states have only deregulated either electricity or natural gas (not both), while others have allowed for partial choice whereby only select groups of customers have the ability to choose, often for piloting purposes. The figure below shows the current status of deregulation by state, as of January 2016.

Electricity and Natural Gas Restructuring By State

Source: Various State PUCs